On credibility and penalties – Nearly Legal: Housing Law News and Comment, 31 October 2022

Lowe v Charterhouse (2022) EW Misc 8 (CC)

A county court deposit penalty claim judgment, but well worth noting because a) a Circuit Judge decision by HHJ Luba KC, b) there are some broader points in application , and c) well it is quite the case.

Mr Lowe was the tenant of the Governors of Sutton’s Hospital in Charterhouse (a charitable foundation which owns and lets historic buildings around Charterhouse Square in London). Mr Lowe’s first tenancy began on 4 January 2010 (the date is significant) with a rent of £2384 per month and a deposit of £3300. There were subsequent statutory periodic tenancies, and fixed term tenancies up to a fixed term agreement from 31 July 2014 to 31 July 2015 and a subsequent statutory periodic tenancy arising on 1 August 2015. These amounted (following Superstrike) to 8 tenancies overall. Mr Lowe alleged, but Charterhouse denied, that there was a further fixed term agreed ending 30 Sepember 2017 and a subsequent statutory periodic tenancy, so 10 tenancies overall.

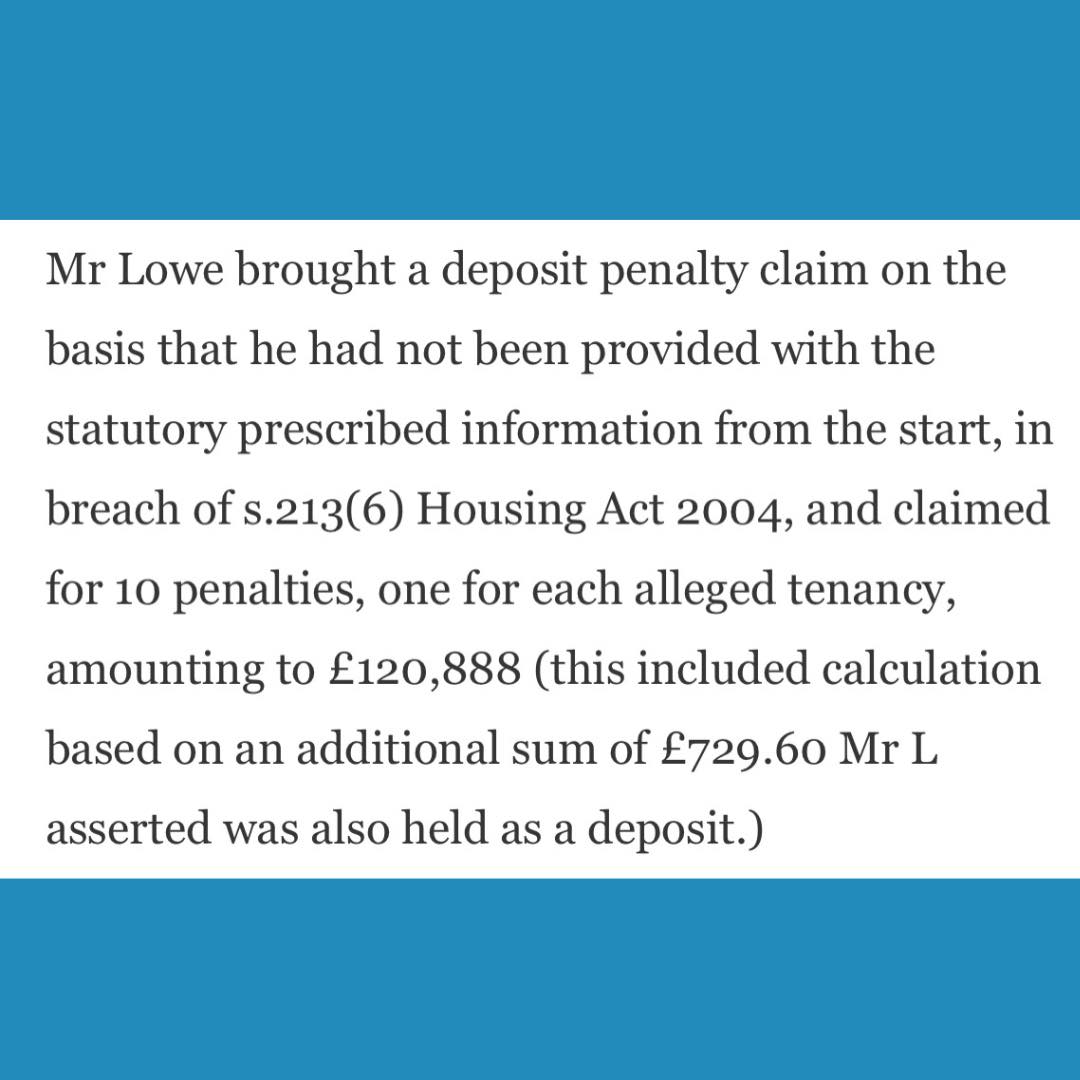

Mr Lowe brought a deposit penalty claim on the basis that he had not been provided with the statutory prescribed information from the start, in breach of s.213(6) Housing Act 2004, and claimed for 10 penalties, one for each alleged tenancy, amounting to £120,888 (this included calculation based on an additional sum of £729.60 Mr L asserted was also held as a deposit.)

I will spare you the tension of reading to the end for the outcome. Mr Lowe lost entirely. But the why and how are very interesting.

i) Limitation

Charterhouse argued that Mr L’s claim was limited to 6 years before issue, under section 9 Limitation Act 1980, as an action for a sum recoverable by statute. Mr L argued that limitation was 12 years for an action upon a specialty under s.8 Limitation Act. (Apparently it was common ground that a ‘statutory claim’ was an action upon a specialty unless s.9 applied). The claim was issued on 10 June 2021.

S.9 Limitation Act provides

(1) An action to recover any sum recoverable by virtue of any enactment shall not be brought after the expiration of six years from the date on which the cause of action accrued.

HHJ Luba KC held that ‘recoverable’ was not limited to sums paid over and of which recovery was sought.

That Act clearly treats recovery as including the obtaining of money not previously paid out by a claimant to a defendant.

For instance, section 10 addresses recovery of a contribution by A from B towards what A may in future (at least in some cases) be required to pay C or may in the past have paid to C. By way of further example, the interpretation section in the 1980 Act, section 38, speaks of actions to “recover” arrears of interest (or damages in respect of arrears of interest) which plainly are not sums which have already been paid. Section 38(11) also refers to three specific statutes relating to benefits, credits, and contributions where “recovery” and “recoverable” would embrace obtaining monies the claimant has not previously had.

So, a deposit penalty claim was caught by s.9. Mr Lowe’s claim was limited to the period from 10 June 2015 only.

ii) The alleged additional £729.60 deposit.

This was a sum agreed between Mr L and Charterhouse as ‘overpaid’ rent due to a delayed move in date in 2010. There was no evidenced agreement that Charterhouse would hold it as security and there was no intention when it was paid that it would be held as security beyond Mr Lowe’s own evidence. The sum had been repaid to Mr L in 2016. Any decision on this (and other issues below) relied on Mr Lowe’s credibility as a witness.

This provides my opportunity to give my assessment of Mr Lowe’s evidence. I regret that I found him a most unsatisfactory witness. He was dogmatic and inappropriately verbose. He was combative and argumentative in answering questions, being inclined to try and make a point or advance his case at every turn. That did not improve, despite encouragement from the Court that he restrain himself. He was wholly inflexible. In my assessment he has become so absorbed or obsessed by his disputes with his landlord (in this and other tribunals), that he had lost all ability to exercise judgment, insight, objectivity, or flexibility. While I accept that he genuinely believed in the correctness of what he was saying and what he had written (to the extent that he plainly treated his account as the only possible truthful account), and that he was not seeking deliberately to mislead the Court, I considered that I should approach his evidence with a good deal of caution and circumspection.

Given the lack of reference to this sum and supposed agreement in otherwise very detailed discussions between the parties evidenced in the documents, the Court was not satisfied on the balance of probabilities that there was any such agreement as to the £729.60 as security.

iii) Initial protection of the deposit. The deposit was first protected in September 2010. The is was because the tenancy at the start in January 2010 was not an assured shorthold tenancy as it was over the then rent limit. This was to change in October 2010, by Assured Tenancies (Amendment) (England) Order 2010 raising the AST rent upper limit to £100,000 per annum. The evidence of Charterhouse’s agent was that they had planed and protected the deposits beforehand, and sent a letter enclosing deposit certificate, scheme booklet and prescribed information (unsigned, for tenant’s signature and return). There was a copy letter on the file, though not the enclosures.

Mr Lowe’s evidence was that he had not received the September 2010 letter, though his witness statements said that ‘he did not recall’ receiving it.

HHJ Luba KC was satisfied that the letter and enclosures had been sent. The question then was whether this amounted to ‘giving the tenant’ the prescribed information. It might not, but:

It is a strong thing, in a case in which A asserts something was posted to B and B contends that he did not receive it, to find that a Court is satisfied that in fact the documentation was received. But in the instant case I am so satisfied.

As I have indicated above, I did not feel able to treat Mr Lowe (for these purposes, the recipient) as a reliable witness. He moved position from not being able to ‘recall’ whether he received the documentation to giving oral evidence to the effect that he was ‘sure’ he did not.

I take judicial notice of the fact that most post delivered to the postal service is subsequently delivered to the addressee.

In his oral evidence, Mr Lowe invited me to accept that he had known nothing about tenancy deposit protection matters, or the protection of his own deposit, until 2015/16. I regret to state that I did not believe him. I am prepared to accept that he and Charlotte (of the agents) did say something to one another about tenancy deposits in 2015/16 but I am also satisfied that if he had not by that date had what purported to be the required information relating to tenancy deposit protection he would have insisted on its provision.

The court held the information had been ‘given’.

iv) Had the required information been given? This came down to the question of whether the prescribed information met the requirements of Housing (Tenancy Deposits) (Prescribed Information) Order 2007 Article 2(1)(g)(vii)

(vii) confirmation (in the form of a certificate signed by the landlord) that—

(aa) the information he provides under this sub-paragraph is accurate to the best of his knowledge and belief; and

(bb) he has given the tenant the opportunity to sign any document containing the information provided by the landlord under this article by way of confirmation that the information is accurate to the best of his knowledge and belief.

Specifically, the requirement of being ‘signed by the landlord’. The agent’s evidence was that an unsigned copy had been sent for the tenant’s signature and return.

The court held the requirement had been met

a) the certificate provided for the tenant’s signature before the landlord’s. The tenant cold not reply on his own failure to sign and return the certificate.

b) The tenant knew who had sent him the information, that they had signed the covering letter and the letter stated that it enclosed the ‘prescribed information’. The statutory objective had been achieved.

The prescribed information had been given by the landlord’s agent as a specified enclosure to a document signed by an identified individual member of staff of the agent. The certificate and booklet gave the tenant all the information the statute required. It fulfilled the statutory purpose.

This was satisfaction of the requirement as either being ‘substantially to the same effect’ as that prescribed, or by application of a sensible, constructive and purposive approach, following Northwood Solihull Ltd v Fearn (2022) EWCA Civ 40 at (66) to (68) (our note).

A further issue was raised on Mr Lowe’s behalf at trial. The prescribed information is required to include “…the circumstances when all or part of the deposit may be retained by the landlord, by reference to the terms of the tenancy”. The information in this case referred to a clause 6 in this regard, but this did not match Mr Lowe’s tenancy agreement (apparently as it was not originally an AST, so was in different form). The Court held that again, this was either ‘to substantially the same effect’ or saved by a sensible, purposive approach, as per Northwood v Fearn.

v) Was provision of the information in 2010 suffice to be protection for the August 2015 tenancy?

The Deregulation Act 2015 had inserted new section 215B to Housing Act 2004, providing that protection for a previous tenancy counted for subsequent tenancies. But s.215B applies “where the tenancy deposit first received by the landlord was received “in connection with a shorthold tenancy”, described by section 215B(1)(a) as “the original tenancy”.”

Here, the deposit was received for a non-shorthold tenancy in January 2010. Did s.215B have effect? The Court held yes.

Parliament, when enacting the Deregulation Act 2015 must be taken to have known that the ‘ambulatory’ features of the regime of assured tenancies in Housing Act 1988 had been in place for more than two decades. Tenancies could move in and out of assured status and into shorthold status. Its words cannot be used to ossify the treatment of the statutory scheme in its application to a particular tenancy. I am satisfied that section 215B can operate constructively and that the ‘original tenancy’ concept within it can apply to an original tenancy that was at first non-assured and became an assured shorthold and/or to the first statutory periodic assured shorthold tenancy that springs from it.

Such a construction gives effect to Parliamentary intent to address the perceived ‘mischief’ that the decision in Superstrike had given rise to. Namely, the notion of a tenancy deposit been deemed ‘paid’ where no new payment was actually made with the consequence of repeated resurrection of the tenancy deposit obligations under Housing Act 2004. Parliament met that with a suitable deeming of compliance with the tenancy deposit information requirements. Its efforts should not be treated as falling short of the target in cases such as the present.

vi) Was there a new tenancy in October 2015? There was no evidence of a concluded agreement, though there were discussions. Mr Lowe had begun paying an increased rent, but this by itself was not sufficient to establish a new tenancy agreement. The dates given by Mr Lowe were contradicted by the documentary evidence. There was no 9th tenancy, and therefore no 10th statutory periodic tenancy.

vii) Return of the deposit. Charterhouse had attempted to return the deposit by cheque. Mr Lowe had said that he didn’t know how to ‘conveniently’ deposit the cheque with his on line bank, then that the process of doing so was ‘tedious’. He did not provide bank details for a transfer.

vii) Was Mr Lowe entitled to an order for return of the deposit?

This was obiter, as the claim in breach of deposit duties failed. But in any event, this would have failed. There was no pleaded claim for the return of the deposit. The wording of s.214(3) is ““The court must, as it thinks fit, …”. That sensibly admits of a degree of judicial judgment or discretion” on what would appear to be a mandatory direction. Further, here the tenancy was ongoing, and the deposit only held because Mr Lowe had not banked a cheque or provided bank details. This was a paradigm case for refusing to order return of the deposit.

viii) If a penalty had been required on the facts, how much would it have been?

Culpability was the relevant factor, as per Okadigbo v Chan (our note) and Sturgiss v Boddy (our note)

In this case, it would also be relevant that

a. The deposit has been protected since it first required protection;

b. The tenant has known that it was protected;

c. It is (at the date of trial) still held and available;

d. It had (pre-trial) been tendered to the tenant in case he wanted to have it back;

e. Charterhouse is a charity;

f. It employed professional agents to deal with these tenancy matters;

g. Those agents sought to comply with newly applicable legal provisions in 2010 even before they took effect (see my reference above to ‘going the extra mile’); and

h. If they failed to comply with the statutory provisions in relation to prescribed information, it was not in the absence of a genuine attempt to comply.

If there had been an award, it would have been of one times the penalty, the bottom level, so £3300.

Claim dismissed.

Comment

Much of this case turns on the specifics and evidence (or lack of it). But the approach to interpretation of the statutory requirements does suggest that wholly technical breaches of deposit requirements – at least where what was done is to substantially the same effect as the requirements – may not give rise to successful claims.

I also had to smile at this passage of the judgment:

Mr Lowe is an experienced professional man working in the financial arena and who has significant IT skills (as shown by his ability, as early as 2016, to track-change documents and work on PDFs). I simply did not accept his account that using a banking app or finding out from the bank how to deposit a cheque, was beyond his ability to do without inconvenience. He did not bank the cheque because it served him not to do so. But he did not have the candour to admit that fact.